Alternatives to electrification “politically neglected”

The future of the global lubricants market remains uncertain. We are encountering major disruptions that include a drive towards sustainability, a difficult regulatory environment, and the impacts of digitalisation. Distortion of the world order, both economically and politically, is happening before our eyes. What will happen to the market is anyone’s guess.

Speaking at the UEIL Annual Congress in Cannes, France, on 23 – 25 October 2019, Lutz Lindemann, chief technology officer at FUCHS PETROLUB SE, identified sustainability as the preeminent disruptor for European industrial nations. Climate discussions are creating a difficult political and regulatory environment, says Lindemann. Coupled with a weakening of the European project, the European Union is in bad shape, he says.

Europe is committed to achieving ambitious sustainability targets that include becoming carbon dioxide (CO2) neutral by 2050, and 32% renewable energy in 2040. Requirements coming from sustainability, and the need to develop alternative non-fossil fuel sources, will completely change the setup of the lubricant industry over the next 30 years, says Lindemann.

To minimise our CO2 footprint, politicians, legislation and the industry are pushing e-mobility. Electric vehicle spearheads the Netherlands and Norway have already confirmed that no internal combustion engine vehicles will be approved beyond 2025. In China, by law, a battery-driven vehicle quota of 10% must be achieved in 2019, with 12% the following year. Many other nations have voiced similar intentions.

However, Lindemann is critical of the world’s blind faith in electrification. There is too much focus on battery-driven cars, says the FUCHs executive. Political pressures are directing us down the battery electric vehicle (BEV) route — for the time being. Though, automobile manufacturers are in general agreement that this is “not a good decision,” he says. Unfortunately, German automakers no longer possess the necessary influence to alter the current pathway, implies Lindemann. This electric vehicle (EV) dominance poses significant problems for the entire value chain.

E-mobility is not simply a change in the drivetrain of vehicles. With it comes a total upheaval of the value chain of electric drivetrain components, Lindemann says. EV components are completely different from conventional vehicles; not to mention changes in raw material and the energy supply chain. An impending technology shift from vehicle ownership to mobility as a service, and vehicle automation, delivers further trepidation for lubricant businesses. “The next generation is not interested in cars, they are only interested in mobility,” Lindemann says.

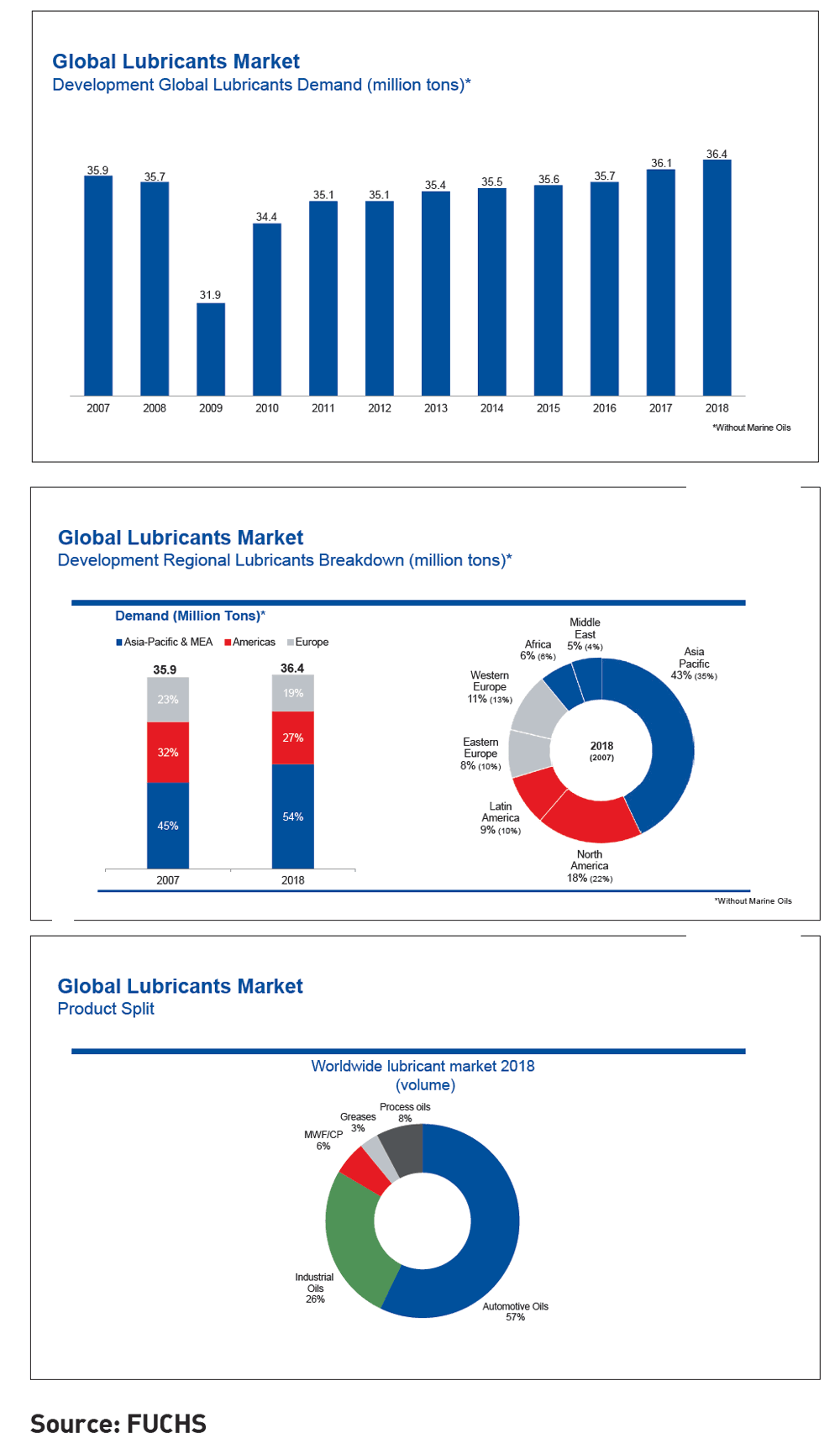

Nonetheless, today’s situation is “not too bad”, says Lindemann. The global lubricants market volume has reached 36.4 million tonnes, and the market continues to expand — dominated by China’s compound annual growth rate (CAGR) of 4.5% since 2007. India is also growing. Though, all other leading lubricant markets, including the United States and Germany, are deteriorating, albeit slowly. The product split is dominated by automotive oils — consisting of 57% of worldwide volumes, followed by industrial oils (26%), process oils 8%, metalworking fluids (6%) and greases (3%).

A transition to BEVs means no more engine oil or transmission fluid. On the other hand, grease requirements are “more or less balanced,” he says, with new requirements for cooling and thermal management balancing decreases in other areas. The value chain will shift towards battery manufacturing, accounting for 60% of the value, says Lindemann, with China leading the way on battery technology. Further declines in lubricant requirements are observed in an estimated 70% reduction in parts to be machined, the increasing use of lightweight materials, and alternative machining processes, such as forming.

While the immediate future is evidently electric, there are several viable alternatives to electric vehicles. The hydrogen economy, including Fuel Cell, ‘Power to X’ and e-fuels, are the real opportunity to save CO2, says Lindemann. Though, alternative technologies to traditional e-mobility are “politically neglected,” he says.

In Europe, the EV fleet includes half a million BEVs (0.2%). A further 400,000 BEV registrations are expected in 2019. To achieve existing sustainability targets, roughly four million new BEVs are required in 2030, says Lindemann, necessitating a 25% yearly increase in new BEV sales. An achievement the FUCHS executive believes is unlikely.

China has stopped subsidies on many BEVs. While BEVs provide a solution to pollution issues in urban areas, Lindemann submits that China is aware battery-driven cars are not the answer to all of their problems. Today, the world’s most populous nation has 1.2 million BEVs, with the expectation of a further 1.2 million in 2020. However, China knows their future is in hydrogen, he says, and has stopped subsidies to focus on hydrogen.

BEV volumes will continue to increase in the medium term. Pricing, technology, infrastructure, and customer acceptance will dictate to what degree, and whether this mobility option persists for the long term. Even assuming a low 20-25% acceptance by 2035, we can expect a significant impact on lubricant volumes.

Lindemann projects a 10% to 20% decline in automotive lubricant demand for the 28 European nations, alongside a 30% fall in metal-processing demand by 2035. Industrial lubricants remain stable in the region, providing an overall European market decline of 10%. The United States will suffer a 20% drop due to efficiency and e-mobility advancements. These declines are offset by 10% growth in China, producing a net 2-3% decline globally.

Lindemann labels the imminent decline in lubricant volumes “not a catastrophe, but a challenge.” More concerning is that the European car industry is not prepared to handle the problem, he says.