Changing landscape of maritime transport

UNCTAD report cites shift towards “new normal”

Approximately 80% of international trade volumes and 70% of the trade value is carried by sea haulage. In 2018, marine trade volumes reached a milestone 11 billion tons, the highest volume ever recorded. While it may appear a time for celebration for shipping companies, even with ongoing increases in volumes, there are signs the tide is turning on maritime trade.

A report from the United Nations Conference on Trade and Development (UNCTAD), published on 22 October 2019, emphasises slowing momentum in maritime trade. The “Review of Maritime Transport 2019” is the 51st annual review of maritime freight, world fleets, rates and markets, ports and the regulatory and legal framework and includes data and events spanning January 2018 to June 2019. During a media event in conjunction with the Global Maritime Forum in Singapore on 30- 31 October, Frida Youssef, chief, Transport Section of Trade Logistics Branch at UNCTAD, and a contributing author, presented the key highlights of the report, which included an overriding theme of rising uncertainty.

The review identified a fall in trade volume growth to 2.7% in 2018, significantly lower than in 2017 (4.1%), and less than the historical average of 3%. Global port traffic growth also weakened, with container port traffic growing at 4.7%, contrasted with 6.7% a year earlier. These changes reflect an unexpected weakening in global merchandise trade growth — both imports and exports — which fell from 4.5% in 2017 to 2.8% in 2018.

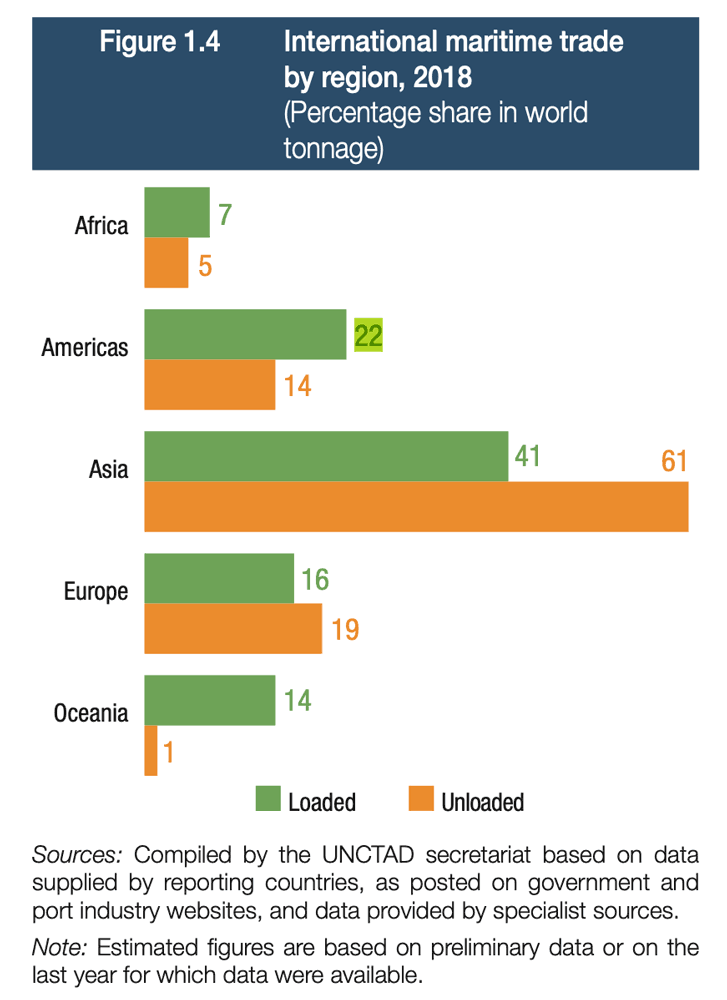

UNCTAD estimates 793.26 million 20-foot equivalent units (TEUs) were handled in container ports around the world in 2018, an additional 35.3 million TEUs over 2017. Asia continues to cater for the majority of container port traffic handling almost two-thirds of global volumes, half of which originates in China, says Youssef.

Alongside a discernible trade slowdown, container fleet supply capacity increased by 5% in 2018 mainly due to the ongoing delivery of mega container ships. An increase in container ship supply is accentuating an already oversupplied market and has impacted freight rates in 2018, says Youssef. Though, the temporary withdrawal of ships to allow for the installation of scrubbers — to ensure compliance with International Maritime Organization’s (IMO) low sulphur regulation — has reduced the oversupply somewhat, she says.

The UNCTAD report identified a series of trends driving the recent dip in maritime trade growth — including mounting concerns around trade policy and increasing protectionism.

The United States’ and China’s standoff is affecting trade flows. Tariff increases implemented in September 2018, May and June 2019 affected almost 2% of world maritime trade volumes, says Youssef. These growing tensions are impacting supply chains, with trade diversion and substitution of suppliers, she says. Recent reports also indicate Chinese goods are moving to new locations such as Southeast Asia. Further geopolitical instabilities, such as Great Britain’s decision to leave the European Union with the possibility of a ‘no-deal Brexit’, are contributing to uncertainty around global trade, says Youssef.

The United States’ and China’s standoff is affecting trade flows. Tariff increases implemented in September 2018, May and June 2019 affected almost 2% of world maritime trade volumes, says Youssef. These growing tensions are impacting supply chains, with trade diversion and substitution of suppliers, she says. Recent reports also indicate Chinese goods are moving to new locations such as Southeast Asia. Further geopolitical instabilities, such as Great Britain’s decision to leave the European Union with the possibility of a ‘no-deal Brexit’, are contributing to uncertainty around global trade, says Youssef.

An economic slowdown and doubts around the world economy are also influencing the maritime landscape. There has been a deceleration in globalisation over the last decade, with political and structural changes to the industry that include greater regionalisation of supply chains and trade flows. These new shipping networks and trade configurations have been developing over a prolonged period, says Youssef. The UNCTAD review also emphasises the greater role of new technology and services in value chains and logistics within the industry.

A rebalancing in China’s economy, more frequent natural disasters and climate-related disruptions, supply-side disruptions, and weakness in industrial sectors were also cited as influential in falling trade growth over the past year.

A rebalancing in China’s economy, more frequent natural disasters and climate-related disruptions, supply-side disruptions, and weakness in industrial sectors were also cited as influential in falling trade growth over the past year.

An accelerated environmental sustainability agenda will have a major bearing on the shipping industry and is amplifying uncertainty within the sector. The transition to cleaner fuel sources takes a leap forward when the IMO 2020 regulation came into effect on 1 January 2020. The legislation requires a reduction in fuel sulphur content from 3.5% to 0.5% and brings with it environmental benefits. It also creates fresh challenges for the shipping industry.

UNCTAD anticipates a surge in shipping fuel costs as a result of the new regulations, owing to additional costs of compliance. The report predicts an “increase in operating fuel costs and price volatility,” as well as a potential reduction in supply capacity. There is a high likelihood that carriers will look to pass on heightened costs to shippers in various forms, such as a new bunker surcharge formula.

Options for shipping companies to comply with IMO 2020 include transitioning to cleaner fuels or retrofitting ships with exhaust gas cleaning systems or “scrubbers”. Liquefied natural gas (LNG) is expected to be one of the main fuels in an ongoing push for improved fuel economy, says Youssef.

A significant expansion in the LNG sector has resulted in LNG carriers delivering the highest growth rate in the 12 months to January 2019, at 7.25%, although bulk carriers, oil tankers and container ships completed higher volumes of ship deliveries. UNCTAD suggests the trend to LNG will continue alongside mounting environmental concerns within the shipping industry and a need to promote cleaner energy sources.

A significant expansion in the LNG sector has resulted in LNG carriers delivering the highest growth rate in the 12 months to January 2019, at 7.25%, although bulk carriers, oil tankers and container ships completed higher volumes of ship deliveries. UNCTAD suggests the trend to LNG will continue alongside mounting environmental concerns within the shipping industry and a need to promote cleaner energy sources.

Despite a contraction in growth amid heightened uncertainty, the UNCTAD report continues to project above-average growth in international maritime trade over the next few years, with an average annual growth rate of 3.4% from 2019–2024. Containerised, dry bulk and gas cargoes will impel growth during this period.

Positive developments underpinning this growth forecast include China’s Belt and Road Initiative, new bilateral and regional trade agreements, and opportunities arising from the global energy transition.

Youssef also noted a confluence of events that have culminated in a “new normal” for the maritime landscape, beginning with the global recession of 2009. A slowing of the market economy and trade growth, China’s evolution from manufacturing to an increasing focus on services, and regionalisation of trade flows, accelerated environmental agenda, the energy transition, and the greater role of next generation technologies, are all impacting the global supply chain, says Youssef.

echo '