Downstream outlook: Global demand growth exceeds expectations

Refining demand growth has exceeded market expectations with 1.6 million barrels per day (MMb/d) of product demand added in 2017 compared to 1.2 MMb/d the previous year, according to McKinsey Energy Insights report on the ‘Global Downstream Outlook’ published in August 2018 by McKinsey & Company. China (40%) and OECD Europe (20%) have delivered the lion’s share of the growth, which has been attributed to a broad global economic recovery — particularly in the second half of 2017, and a modest rise in capacity.

McKinsey identified diesel/gasoil demand increases in the industrial and transport logistics sectors as influential — the 2016 decline of 120 thousand barrels per day (Kb/d) supplanted by 500 Kb/d growth in 2017. Asia contributed almost 500 Kb/d of new distillation capacity out of a global total of 585 Kb/d, the majority of which occurred in China and India. The ‘Global Downstream Outlook’ also noted that unplanned disruptions in Mexico, the U.S., and Europe kept market supply tight throughout 2017.

McKinsey identified diesel/gasoil demand increases in the industrial and transport logistics sectors as influential — the 2016 decline of 120 thousand barrels per day (Kb/d) supplanted by 500 Kb/d growth in 2017. Asia contributed almost 500 Kb/d of new distillation capacity out of a global total of 585 Kb/d, the majority of which occurred in China and India. The ‘Global Downstream Outlook’ also noted that unplanned disruptions in Mexico, the U.S., and Europe kept market supply tight throughout 2017.

The report highlighted strong performance in Asia as margins rose USD1.5/barrel in 2017, though these margins have dipped slightly at the start of this year. Favourable utilisation and margins are the results of strong product growth. In particular, the report observes transport fuels demand driving positive hydroskimming margins in Northeast Asia for most of the second half of 2017.

European refiners also benefitted from strong margins — rising on average by ~USD2.15/barrel after an uninspiring 2016 — and utilization rates (86%) were at the highest level since 2006. On the U.S. Gulf Coast (USGC), cheaper and readily available local crude helped boost margins and left USGC refiners working tirelessly to meet export market demand. The report confirmed cracking margins for light sweet crude were up ~USD3/ barrel in 2017 compared with 2016.

A positive outlook was offered for global refining to 2020, Energy Insights predicting an average annual increase in global demand of 1.3%. Capacity increases will continue to be driven by Asia, the majority of which come online in 2019, and the world’s fastest-growing economies from Asia will continue to propel global demand growth. Asia’s 2018 and 2019 refining utilisation will remain consistent with 2017 performance, a further increase expected in 2020 owing to high distillate demand globally.

New refining capacity added in 2018 is expected to impact European hub utilisation in 2019, with a forecast fall of 10%. However, a 2020 rebound is anticipated as European refiners benefit from a global increase in marine gasoil demand following the implementation of the International Maritime Organization’s (IMO) MARPOL Annex VI regulation from January 1, 2020, that seeks to cut sulfur emissions in the shipping industry. Utilisation will “likely rise to ~92% with hydroskimming capacity setting prices on the margin.”

USGC market utilization is projected to rise slightly in 2018 and 2019, based on a strong outlook for global demand. The aforementioned new bunker fuel specifications in 2020 are expected to boost utilization above 90%.

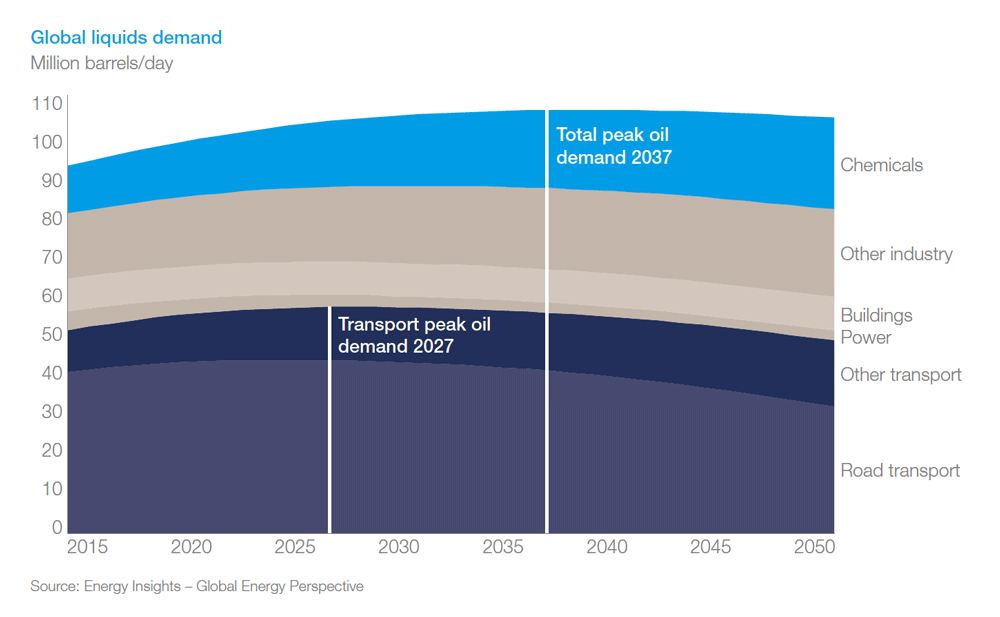

Beyond 2020, a somewhat bleaker picture is emerging for refiners. A “deceleration and eventual decline in demand” will place pressure on utilization and margins from 2025 with new technologies and changes to consumer behaviour the key drivers.

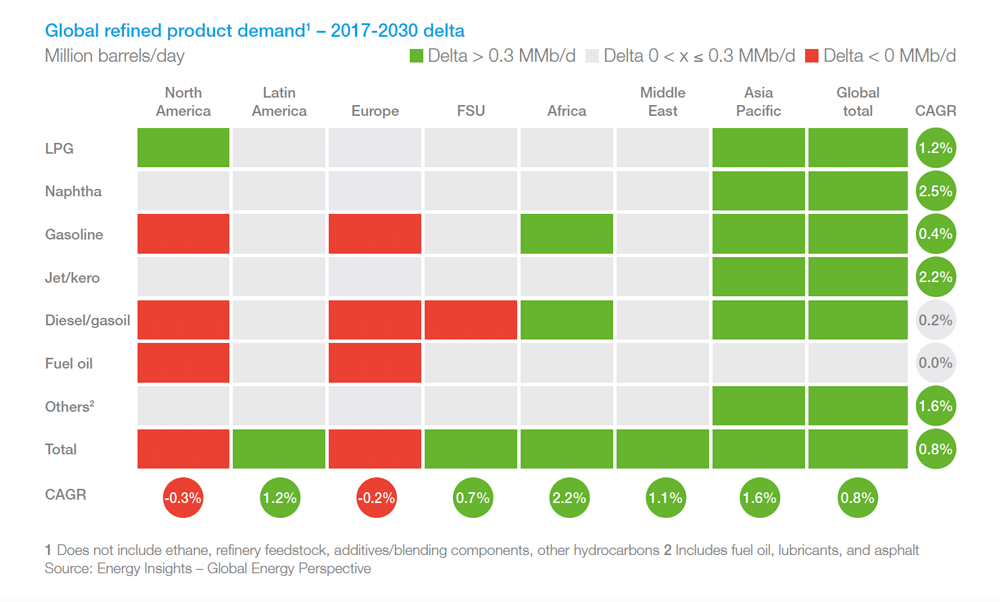

Growth in Asia is expected to decelerate to an average 1.6% per annum (p.a.) to 2030, significantly lower than the 2-3% p.a. observed from 2010-2017. North America and European demand is likely to fall between 2020-2025, driven by peak car ownership and electrification. Europe faces progressive declines in utilization from 2020 due to slowing demand growth and growing global capacity. The report’s authors signposted that transport sector oil demand will peak before 2030, although total liquids demand is not expected to summit until 2037, at which point demand growth in the chemical and industrial sectors will begin to slow.

IMO’s MARPOL Annex VI regulation requires ships outside the emission control area (ECA) regions to operate on fuels with less than 0.5% sulfur content by January 2020. The current limit is 3.5%. The rollout is expected to “increase global refining utilization, tighten distillate markets, and widen light-heavy differentials, bringing the potential for a very sharp improvement in margins, especially for high-conversion refiners.” Energy Insights suggests the regulation will impact ~3 MMb/d of high-sulfur fuel oil demand in bunkers — a staggering~80% of the shipping sector fuel demand.

Share of product demand met by crude oil will decline slightly moving forward as NGLs (i.e., propane, butane, and light naphtha from gas processing) are forecast to account for 10% of total product supply by 2025, and other non-oil sources such as biofuels, pygas, CTL/GTL, and MTBE — will also continue to rise. Energy Insights projects a 3% shift to light crude grades (>35 API) by 2030 — attributed to growing U.S. light tight oil (LTO) or unconventional oil production.

Share of product demand met by crude oil will decline slightly moving forward as NGLs (i.e., propane, butane, and light naphtha from gas processing) are forecast to account for 10% of total product supply by 2025, and other non-oil sources such as biofuels, pygas, CTL/GTL, and MTBE — will also continue to rise. Energy Insights projects a 3% shift to light crude grades (>35 API) by 2030 — attributed to growing U.S. light tight oil (LTO) or unconventional oil production.

An increase in distillation capacity is the result of a few big projects in Asia and the Middle East, however, several other greenfield investments are planned including Turkey’s 214-Kb/d Aliaga refinery and Dangote’s 500-Kb/d greenfield refinery in Nigeria. Conversion capacity is the more prominent trend though, with twice the rate of distillation capacity growth anticipated to 2020 — which will improve overall average complexity and light product yield.

A drop in domestic transport demand will result in North America transitioning from a net gasoline importer in 2017 to a net exporter post-2025. Growing shorts in China, India, and Southeast Asia will result in Asia converting to a net importer after 2020. The Middle East will assume the position of the third-largest gasoline exporting region from 2020, with the majority of products equipping South and Southeast Asia.

Asia-Pacific and Africa will witness the largest increase in net distillate imports by 2030. Energy Insight predicts Asia’s diesel/gasoil net deficit will grow slightly by 75 Kb/d from 2017 to 2030, attributed to higher demand in India, Southeast Asia and Oceania. Africa will experience a more substantial increase in net imports of 400Kb/d between 2017-2030, courtesy of USGC, Middle East, and India’s supply. The Middle East and the Former Soviet Union will continue to be the largest net exporters by 2030, while lower domestic consumption will reduce European net imports beyond 2025.