Powerfuels: Missing piece in the global energy jigsaw puzzle?

The 2018 World Energy Outlook is the most recent global energy forecast released by the International Energy Agency (IEA). The Outlook provides a mid-range prediction that global energy demand will grow by 3,743 million tons of oil equivalent (Mtoe), or 27%, from 2017 to 2040. This “New Policies Scenario” is propelled by growth in the world’s developing countries whose share of global demand will reach 70% by 2040.

While availability, affordability and security of energy supply are key considerations in ongoing energy requirements; perhaps the most significant challenge is decoupling ever-increasing energy consumption from fossil fuels and their lingering greenhouse gas emissions. An April 2019 report, published by Global Alliance Powerfuels (GAP), suggests alternative (renewable) energies will account for more than 40% of growth in energy demand, with China and India leading the charge. “Eco-energy” will deliver 14% of global energy supply by 2040.

A shift to electrification will play a dominant role in this energy transition with electric vehicles and heat pumps two areas likely to stimulate sustained electricity demand. The GAP report, entitled Powerfuels: A missing link to a successful energy transition, estimates electricity’s contribution of final energy will sit between 32% and 47% in the United States by 2050, based on a variety of differing scenarios.

However, despite electrification contributing to the lion’s share when it comes to renewable energy options; the final solution is likely to include a myriad of technologies. One thing is for sure, direct use of electricity from renewable sources will be unable to satisfy 100% of energy requirements in the foreseeable future.

The Global Alliance Powerfuels is a cross-industry coalition of international companies and associations from the energy, automotive, aviation, chemical, petroleum and engineering sectors. The group believes powerfuels are the “missing link” in this energy transition. GAP was formed at the end of 2018 by the German Energy Agency (dena) and 16 high-profile founding members that include: Shell, Bosch, Audi, Daimler and the Mitsubishi Corporation. The organisation’s goals are to raise awareness of powerfuels and to encourage the development of regulatory frameworks that foster the advancement of these fuels.

Powerfuels are defined as “synthetic gases and liquid fuels produced from Power-to-X processes by utilising renewable electricity.” The electricity-based fuels are sometimes referred to as e-fuels; though, this naming convention can distort their application as solely bound for the mobility sector.

A climate-friendly alternative to fossil fuels, powerfuels have the potential to accelerate the de-fossilization of many industries. Like fossil fuels, powerfuels are energy dense, a distinct advantage over electricity, and ideal for instances where high amounts of energy are required. Molecular equivalence to their fossil fuel rivals allows the utilisation of existing infrastructure for transportation, distribution and storage, such as via oil and gas pipelines, storage facilities, and refinery equipment.

However, it is the tradeable and transportable nature of these gaseous and liquid energy sources that makes powerfuels the “necessary missing building block for the energy transition,” says GAP. Not only does this allow new carbon-neutral export opportunities, it can diversify supply for energy importers.

In many sectors direct electrification is impractical and viable alternatives to fossil fuels are fledgling, such as aviation, maritime shipping, non-electrical rail transport, heavy-duty long-distance road transport or the use of heavy machinery in sectors such as mining and construction.

Even with an imminent increase in electricity generation from renewable sources, availability of powerfuels provides security of supply. Unpredictability of natural elements such as wind and sun, and concerns around the stability of electricity grids in some markets, have been recognized as trepidations for the growth of renewable electricity.

GAP’s initial lobbying efforts will focus on Europe as a region of demand for powerfuels. However, the fuels provide a viable solution for any country “which possess abundant space and good conditions for renewable power.” Estimates from the World Energy Council – Germany suggest powerfuels could reach 20% of current fossil fuel demand by 2050, or 20,000 TWh, the majority of which will likely occur in sectors unable to employ direct usage of renewable electricity.

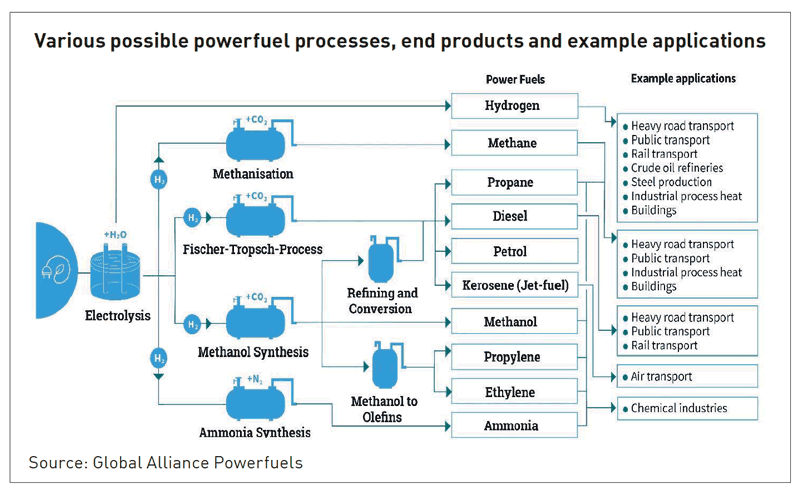

Technologies for powerfuel production are market-ready, says GAP. Irrespective of the end product, electrolysis is the preliminary step — using electrical energy to split water into hydrogen and oxygen. Succeeding processes include methanisation, Fischer-Tropsch-Process, Methanol Synthesis or Ammonia Synthesis and produce hydrogen, synthetic gas (e.g. methane, propane), and synthetic liquid fuels and chemicals (e.g. methanol, diesel fuel, gasoline, kerosene, ammonia, Fischer-Tropsch products).

Technologies for powerfuel production are market-ready, says GAP. Irrespective of the end product, electrolysis is the preliminary step — using electrical energy to split water into hydrogen and oxygen. Succeeding processes include methanisation, Fischer-Tropsch-Process, Methanol Synthesis or Ammonia Synthesis and produce hydrogen, synthetic gas (e.g. methane, propane), and synthetic liquid fuels and chemicals (e.g. methanol, diesel fuel, gasoline, kerosene, ammonia, Fischer-Tropsch products).

Nonetheless, the emergence of powerfuels is not a done deal yet. Despite the obvious benefit of a green “drop-in” alternative to fossil fuels that can utilise existing infrastructure, powerfuel production plants are capital intensive, with high fixed and low marginal costs. Though, the GAP report suggests there is “considerable scope for future cost reductions through economies of scale.” Electricity costs generate the largest portion of powerfuel costs, followed by carbon capture. Costs vary widely based on the type of fuel produced.

Investment in water electrolysis is a key consideration. Based on historical trends, GAP projects the cost of electrolysers will fall over the coming decades. Investments are likely to reach USD40 million per year between 2018 and 2020. A significant scale-up of plant size is paramount to decrease in investment costs and avail of economies of scale. Annual worldwide electrolyser capacity has been below 20MW per year from 2010 to 2017.

When assessing the viability of powerfuel production, costs must be calculated using “cradle to grave costing,” says GAP. When system-level costs are considered, the fuels offer a “lower total cost pathway that is complementary in nature to the other energy transition approaches.” When evaluating based on a tank-to-wheel basis, critical cost components are ignored, and true energy system costs are not captured.

Despite significant local and export opportunities for powerfuels from countries that possess the necessary renewable energy sources, the GAP report calls for policies that recognise the carbon-neutral nature of powerfuels and will stimulate demand over their fossil fuel equivalents.

echo '