Shipping: no clear-cut path to decarbonisation

Tightening regulations on the use of sulphur in the maritime industry went into effect on 1 January 2020. The implementation of the MARPOL Annex VI regulation by the International Maritime Organization (IMO) requires all shipping companies to limit their fuel sulphur content to 0.50% when operating outside of Emission Control Areas (ECA).

This was a significant change to the regulatory framework and will have a major impact on the estimated 90,715 ships around the globe. Currently, 82% of the sector’s energy needs are satisfied using high sulphur heavy fuel oil, with marine gas and diesel oil making up the balance of shipping fuel requirements.

This was a significant change to the regulatory framework and will have a major impact on the estimated 90,715 ships around the globe. Currently, 82% of the sector’s energy needs are satisfied using high sulphur heavy fuel oil, with marine gas and diesel oil making up the balance of shipping fuel requirements.

The expectation is that the owners of large vessels, such as oil tankers, containers and bulk carriers, will make the switch to very low-sulphur fuel oils and alternative fuels such as liquefied natural gas (LNG) and methanol. Otherwise, shipping companies are likely to retrofit vessels with exhaust gas cleaning systems or “scrubbers” to enable the ongoing use of high sulphur fuels, while avoiding sanctions. Scrubbers are designed to remove sulphur oxides from the ship’s engine and boiler exhaust gases. Bulk and container carriers, oil and chemical tankers make up one-fifth of the worldwide shipping fleet but are responsible for 85% of shipping sector greenhouse gas (GHG) emissions.

While the actions taken by shipping owners are intended to reduce sulphur emissions, the IMO legislation is also expected to be a significant driver in the reduction of carbon dioxide (CO2) emissions in the shipping sector as most commercial vessels are powered by fossil fuels. Though, the actual impact on GHG emissions will depend on the method chosen by shipping companies to reduce sulphur emissions and will not necessarily support CO2 reduction.

The shipping industry is a major contributor to emissions, releasing almost 3% of global CO2 emissions and 9% of CO2 emissions associated with the transport sector. More than 80% of international trade traverses the world via maritime shipping, with a global fleet capacity of nearly two gigaton (Gt). The International Monetary Fund (IMF) has projected that trade volumes will continue to grow at 3.8% annually over the next five years.

Admittedly, shipping is a less carbon intensive transport method than other forms. However, the sheer volume and distances covered by these large vessels present a worrying trend for combating climate change. From 2000 to 2017 the shipping sector increased its emissions by 1.87% annually. IMO has indicated that emissions could rise between 50% and 250% by 2050 with no mitigation action.

Thankfully, efforts are being made to curb shipping sector emissions. Aside from the impending legislation, IMO has previously signalled its intentions on the reduction of carbon emissions. In April 2018, the organisation announced a target to reduce carbon emissions in 2050 by 50% from 2008 levels. IMO also highlighted efforts to reduce the carbon intensity of ships via more energy-efficient design, and improvements to the supply infrastructure.

Preliminary findings in a recent report from the International Renewable Energy Agency (IRENA), released in September 2019, suggest that short-term solutions are insufficient to achieve IMO’s 2050 goal. IRENA is an intergovernmental organisation that supports countries in their transition to a sustainable energy future. The Abu Dhabi-based organisation is optimistic of the sector’s ability to significantly reduce CO2 emissions by 2050; however, the report suggests there is currently “no clear cut path to decarbonisation.” Reducing the carbon footprint is likely to involve a combination of approaches including alternative fuels — based on renewable energy sources, improvements to onshore infrastructure, and increasing operational efficiency to reduce fuel demand.

The IRENA report, “Navigating the way to a renewable future: Solutions to decarbonise shipping” was launched during one of the media events at the Global Maritime Forum held in Singapore in late October. A framing report, the paper is designed to help understand the current status, fuels used and key opportunities to reverse carbon trends.

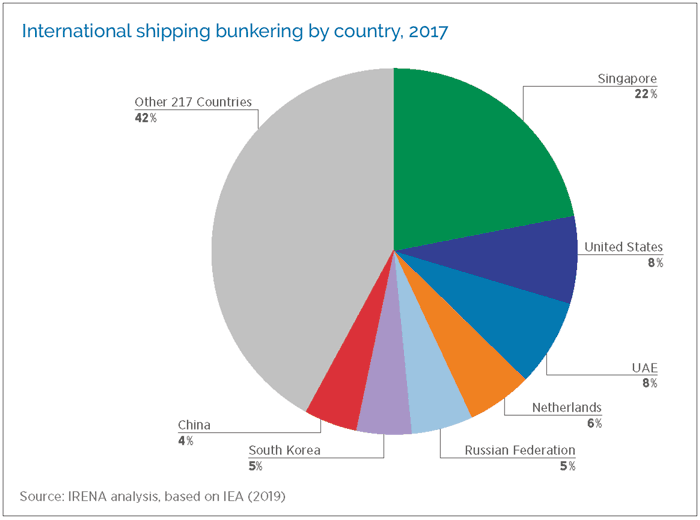

Transitioning from fossil fuels to alternative fuels is not as simple as it perhaps sounds. Replacing heavy fuel oil (HFO) with clean fuel involves the retrofitting or replacement of around 25,000 ships and adjustments to refuelling structures in around 100 ports, that reflect 80% of global freight. Though, the report notes that just seven ports are responsible for nearly 60% of global bunker fuel sales.

Fuel price and the availability of fuels in the logistics of shipping was identified as a decisive factor in decisions around propulsion technology, though infrastructure adaptation costs and ongoing sustainability concerns are also key considerations. Renewable energies are becoming more prevalent and more affordable; however, the IRENA report suggests lower pricing on alternative fuels is necessary to enable widespread adoption.

Fuel price and the availability of fuels in the logistics of shipping was identified as a decisive factor in decisions around propulsion technology, though infrastructure adaptation costs and ongoing sustainability concerns are also key considerations. Renewable energies are becoming more prevalent and more affordable; however, the IRENA report suggests lower pricing on alternative fuels is necessary to enable widespread adoption.

In recent times, LNG has gained increasing popularity as an alternative to HFO. LNG is still a fossil fuel and emits CO2 but is cleaner than HFO and may be suitable in lowering emissions. Nevertheless, to achieve decarbonisation of the shipping industry fuels must be CO2 emissions free and come from carbon-free sources, says IRENA.

LNG is a lower cost fuel than HFO, though the upfront costs associated with retrofits are a key barrier to switching. Consequently, users often opt for distillate fuels, such as marine gas oil and marine diesel oil, as a replacement for HFO. This ensures compliance with IMO 2020, but it does not deliver the same reductions in CO2. Higher costs are a concern, however.

The IRENA report offers a variety of alternative fuel choices including conventional and advanced biofuels; other synthetic fuels, such as methanol, hydrogen and ammonia (NH3); and battery-powered electric propulsion. The report also reviews the merits of renewable sources, such as solar and wind. Despite apparent advantages and disadvantages for each of these options, the authors suggest there is no clear frontrunner in the decarbonisation of the sector.

Biofuels are ready to be used in numerous applications with little or no infrastructure changes and can provide an immediate impact on CO2 emissions. Biodegradability, and environmental safety in the case of spills (when unblended), are key benefits. Unfortunately, the cost of biofuels is approximately twice that of its fossil-borne counterparts and availability is limiting adoption. The report suggests biofuels will become price competitive by 2040, while emphasising that sustainability issues, such as competition for biomass feedstock, could impact biofuel pricing.

Biofuels are ready to be used in numerous applications with little or no infrastructure changes and can provide an immediate impact on CO2 emissions. Biodegradability, and environmental safety in the case of spills (when unblended), are key benefits. Unfortunately, the cost of biofuels is approximately twice that of its fossil-borne counterparts and availability is limiting adoption. The report suggests biofuels will become price competitive by 2040, while emphasising that sustainability issues, such as competition for biomass feedstock, could impact biofuel pricing.

Production of synthetic fuels from electricity, or electrolysis, is known as power-to-liquids. Methanol, hydrogen and ammonia are alternative fuels produced via power-to-liquids process with the potential to replace fossil fuels. Electricity used to produce the fuels must be from renewable sources, otherwise emissions are simply transferred upstream rather than avoided. These fuel products are referred to as e-fuels.

The IRENA paper identified a small number of methanol-powered commercial vessels in operation that produce considerably lower emissions than conventional marine fuels. Retrofitting these vessels is a relatively simple process as the liquid’s properties mean it is more compatible with existing infrastructure, allowing storage in regular non-pressurised tanks. Unfortunately, production costs are also considerably higher than existing marine fossil fuels, and methanol occupies substantially more space than marine fossil fuels, making large-scale implementation difficult.

Blue hydrogen refers to the production of hydrogen with CO2 capture and is the lowest cost hydrogen production method. Some see blue hydrogen as a transitional solution, given the current high costs of producing hydrogen from renewable power. The better solution, though, is green hydrogen from renewable sources, as this is the only source of zero carbon hydrogen. Hydrogen costs are much higher than the fossil fuels in use at this time, though they are projected to become cost competitive by 2030.

Ammonia is not currently used in shipping applications but is being considered as an alternative marine fuel due to its potential for CO2 reduction. Global production volumes of ammonia is around 200 million tons per year — for use in other applications. As with most alternative fuels, ammonia production costs are uncompetitive, and it remains a developing technology. Key concerns include cost, safety and the need for modifications to bunkering and storage (to refrigerate or pressurise). However, the energy agency suggests ammonia is a more attractive option than direct hydrogen due to lower overall capital costs and may become a competitive option in the long term.

Ammonia is not currently used in shipping applications but is being considered as an alternative marine fuel due to its potential for CO2 reduction. Global production volumes of ammonia is around 200 million tons per year — for use in other applications. As with most alternative fuels, ammonia production costs are uncompetitive, and it remains a developing technology. Key concerns include cost, safety and the need for modifications to bunkering and storage (to refrigerate or pressurise). However, the energy agency suggests ammonia is a more attractive option than direct hydrogen due to lower overall capital costs and may become a competitive option in the long term.

Battery technology is advancing rapidly, and we are witnessing increasing use of lithium-ion batteries in transportation. This zero-carbon propulsion method offers an option for smaller vessels on short journeys, though concerns remain over the flammable nature of lithium-ion electrolytes, and high- and low-temperature operation. To mitigate the flammable nature of lithium-ion batteries, the inclusion of lithium-ion storage in vessels must involve a robust battery management system, coupled with thermal management components (e.g. temperature sensors and a cooling system), adequate ventilation to avoid flammable and toxic gases, and fire protection and heat dissipation units in the battery bank chamber.

Wind and solar applications offer the ability to enhance efficiency in shipping — allowing reduced fuel consumption. Cargo space limitations and surface availability are cited as a primary issue for wind, and environmental salinity issues pose a problem for solar PV technology.

While these solutions offer a variety of paths to the decarbonisation of maritime shipping, the shift to zero carbon energy comes with a significant price tag. A new study by UMAS and the Energy Transitions Commission for the Getting to Zero Coalition has estimated a cumulative investment between 2030 and 2050 of approximately USD1-1.4 trillion in order to halve emissions by 2050. The largest share of the investment is required in land-based infrastructure and production facilities for low carbon fuels, according to the report. The Getting to Zero Coalition is a partnership between the Global Maritime Forum, the Friends of Ocean Action, and the World Economic Forum.